1

Feature Story

Alphabet's Discounted Valuation Is an Antidote to Tariff Risk

Feb 04, 2025 · financialpost.com

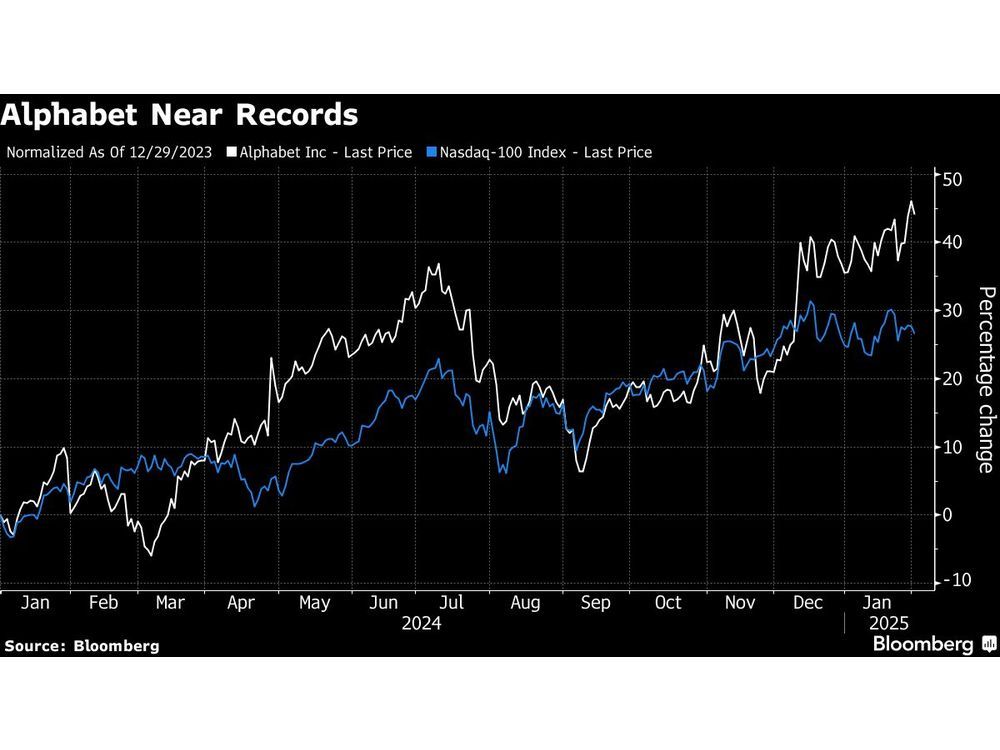

The article also notes that Alphabet's stock has outperformed the Nasdaq 100 Index, maintaining a lower valuation due to competition in AI and antitrust pressures. However, its high-margin businesses, including cloud services and YouTube, act as stabilizers against potential volatility. The company's revenue growth is projected to increase, supported by positive signals from the online advertising market. Alphabet's diverse portfolio, including its AI and self-driving units, adds to its long-term value, with analysts viewing these segments as significant contributors to its overall worth.

Key takeaways

- Alphabet Inc. is seen as a bargain among megacap tech firms due to its durable growth and attractive valuation, despite geopolitical uncertainties.

- China has announced a probe into Alphabet's Google for alleged antitrust violations, focusing on the dominance of Google's Android operating system in China's smartphone sector.

- Alphabet's revenue growth is expected to accelerate to 17.8% in 2025, with net earnings projected to grow by 12%.

- High-margin businesses like Google Cloud and YouTube are considered "shock absorbers" against market volatility and potential tariff impacts.